From Digital Transformation to AI Transformation in Finance and Insurance

For years, the financial and insurance sector has talked about “digital transformation.” Initially, this meant moving from paper to electronic processes, implementing modern core systems, and digitizing the customer experience. But now a more ambitious phase is emerging: a transformation driven by artificial intelligence (AI). In other words, plain digitalization is no longer enough by itself – AI is redefining how banks and insurers operate internally, especially in back-office processes that have traditionally been manual and document-heavy.

Business leaders recognize this changing paradigm. The vast majority see generative AI as key to reinventing operations at scale and speed. In fact, a recent Accenture study found 92% of C-suite leaders believe generative AI is critical for reinvention at scale (source accenture.com). In other words, the much-touted “digital transformation” is evolving into an AI-powered transformation, where intelligent automation sets the pace.

From Digital Transformation to AI Transformation: What’s Changed?

Digital transformation laid the groundwork: it converted physical processes to digital, opened online channels, and improved customer experience. However, many of those digitized processes still followed the same old manual logic – just on a screen instead of paper. Now, an AI-driven transformation goes a step further. It’s no longer just about digitizing existing workflows, but about reimagining those processes with smart algorithms.

For example, under digital transformation, an employee might key data from an application form into a system (still a manual task, just using a computer). Under AI transformation, a trained AI model can automatically read a scanned document, extract the key information, and even make initial decisions without human intervention. The task isn’t merely digitized, but augmented by intelligence. This new AI layer means systems don’t just execute tasks; they also learn, analyze, and continuously optimize those tasks. The result is a smarter, more efficient organization capable of better financial performance. In essence, AI adds a new wave of automation and promises to make banks and insurers more “intelligent” in their operations – more cost-effective and more agile in delivering value.

Industry consultants highlight this shift. Deloitte observes that many companies are moving “from experimentation to strategic implementation” of AI in core business areas, and are achieving significant returns on those investments (source deloitte.com). In other words, AI is no longer an isolated lab experiment; it’s becoming a central engine of transformation. Among leading organizations, AI is now part of their operational DNA. McKinsey even warns that to capture the full value, institutions must aspire to become “AI-first organizations” – integrating AI across all processes – or risk falling behind more daring competitors. This means infusing AI broadly and deeply (not just in one or two projects), essentially making AI the default approach to problem-solving and process design across the enterprise.

The Back-Office: The Last Frontier of Intelligent Automation

Within this AI revolution, the back-office of banks and insurers plays a starring role. It’s in these internal support operations where many manual processes and unstructured document flows still survive – areas that earlier waves of digitalization never fully automated. Consider domains like policy issuance and claims processing, loan administration, customer identity verification (KYC), credit file management, reconciliation of accounting documents, or regulatory compliance. These are critical business tasks rife with forms, contracts, invoices, images, emails – information that must be read, interpreted, and processed by people.

Why have these tasks lagged behind? Mainly because they involve unstructured information: free-form text, scanned documents, photos, PDFs, emails. Until recently, computers didn’t “understand” this messy, non-uniform data very well. Digital transformation allowed companies to store and transmit such content electronically, yes, but not truly comprehend it. That’s why many insurers and banks still needed armies of analysts to review documents, cross-check data between systems, and perform follow-ups manually.

This is where intelligent document processing and automation comes into play, powered by AI. Technologies like IDP (Intelligent Document Processing) combine computer vision, machine learning, and natural language processing to read and understand documents with remarkable accuracy, approaching human-level comprehension. A well-trained IDP system can ingest a mountain of diverse forms – say, insurance claims or loan applications – and automatically classify them, extract relevant data from each, validate it against internal databases, and trigger actions, all in seconds. Tasks that once took minutes or hours of manual work now happen automatically, 24/7, with minimal errors. In practice, document processing automation uses AI, ML, OCR (optical character recognition), and automated workflows to transform how businesses handle documents – automating the capture, processing, and management of information in all types of documents from invoices and contracts to insurance policies and customer records (source danaconnect.com). Employees are freed from the tedium of data entry and verification, and can focus on exceptions or more complex, value-added activities.

Generative AI (GenAI) takes this a step further, not only extracting information but also interpreting and generating useful content for the process. For example, a advanced language model can read through all emails and documents related to a fraud case and produce a concise executive summary for a risk analyst, saving them from reading a hundred pages of reports. Or, given a customer’s information, the AI could draft tailored letters, reports, or emails in a consistent professional tone. In essence, the AI can summarize, contextualize, and even create new text or recommendations, acting as a smart assistant in document-heavy workflows.

For financial firms, this unlocks huge gains in internal efficiency and quality. McKinsey notes that the insurance sector in particular could benefit significantly from generative AI, given the wealth of unstructured data (PDFs, images, Word docs, web pages) it handles and the prevalence of manual tasks in functions like underwriting and claims (source mckinsey.com). In plain terms, insurers and banks are swimming in unstructured information and repetitive processes – precisely the playing field where the new AI excels. Unsurprisingly, in a McKinsey survey of large European insurers, over half expect generative AI to deliver 10–20% productivity improvements, 1.5–3% premium growth, and similar improvement in their loss ratios (source mckinsey.com). A third of those insurers already had GenAI use cases in production, and 20% rated their AI maturity as advanced (source mckinsey.com). The takeaway is clear: the opportunity is real, and the race has begun.

Use Cases: Intelligent Documents in Action

Let’s look at concrete examples of how IDP and AI are redefining key processes in banking and insurance. These cases illustrate why we’re talking about an AI-driven transformation and not just incremental digitalization.

Accelerating Insurance Claims Processing

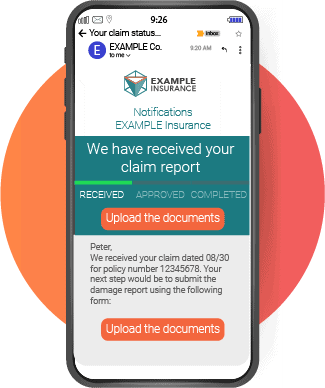

Handling an insurance claim used to involve an adjuster sifting through claim forms, incident reports, damage photos, repair invoices, and then logging everything into a system. It was a slow process prone to errors and bottlenecks (imagine a storm that suddenly generates hundreds of claims at once). With AI, this workflow speeds up dramatically. For example, IDP solutions can automatically read a claim form and extract data like the customer’s name, policy number, incident description, etc. Simultaneously, fraud-detection algorithms can analyze photos or spot suspicious patterns in the narrative. Generative AI can draft a summary of the case or even suggest an initial resolution by comparing it to past similar claims. The human claims adjuster then receives a pre-analyzed file with key details highlighted (for instance, “possible fraud flag on invoice” or “injury likely covered in full”). All this drastically reduces processing time. In fact, some digital insurers today settle simple claims in minutes or even seconds thanks to AI. One insurtech company famously managed to approve and pay out a claim in just 2 seconds – their AI chatbot validated coverage, ran anti-fraud checks, approved the claim, sent payment instructions to the bank, and notified the customer almost instantly (source insurtechinsights.com). Two seconds! While that’s an extreme case, many traditional insurers report 50% or more faster claim handling after introducing intelligent automation. The benefit is not only operational efficiency; it’s also a better customer experience (policyholders get their money faster) and happier employees (freed from drudge work to focus on complex cases or providing a human touch during a claimant’s stressful moments).

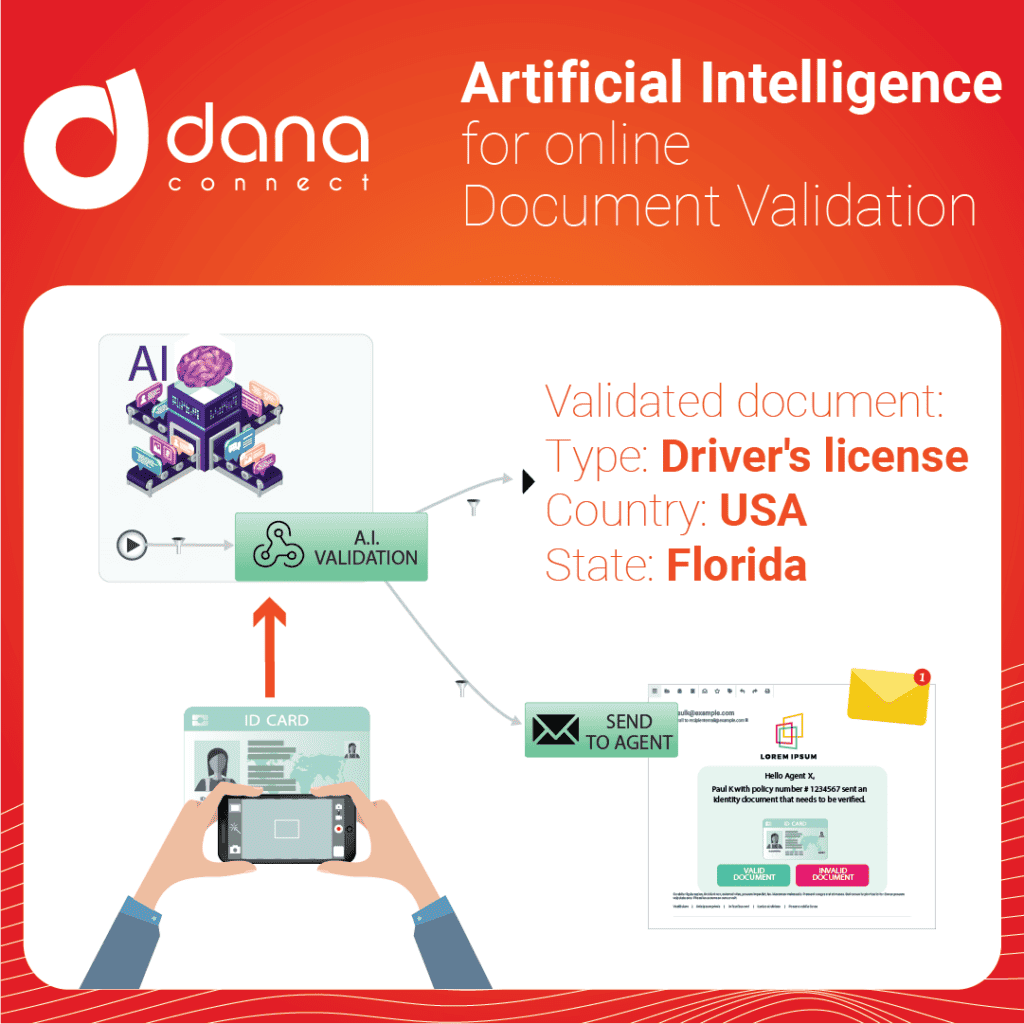

Instant Identity Verification and KYC

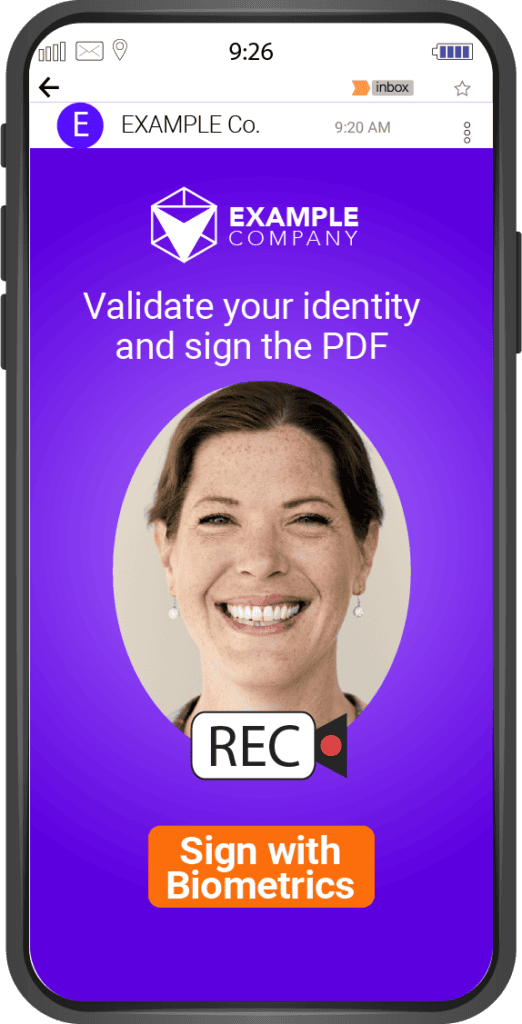

Verifying the identity of new customers – e.g. when opening a bank account or buying a policy – is another critical process that was traditionally paperwork-heavy, slow, and costly. It meant collecting copies of IDs, proof of address, signed forms, then having staff review those documents, type data into compliance systems (KYC/AML), etc. This onboarding could take days, with back-and-forth requests if documents were blurry or missing. Today, by combining OCR, biometrics, and AI, onboarding can be nearly instantaneous. A customer can use their smartphone to snap a photo of their ID and perhaps take a selfie video, and an AI system will automatically extract all the data (name, ID number, expiration date, etc.) and validate it. The AI checks if the ID is authentic, and even compares the ID photo with the selfie to confirm the person’s identity (a liveness check to ensure it’s not a photo of a photo). All of this happens in seconds or minutes without human intervention – unless the AI flags something as suspicious, in which case a manual review can step in. The result: customer onboarding that takes minutes instead of days, with strong compliance. Reports have noted that using video identification and AI, identity verification times have shrunk from multi-day delays to just minutes – keeping customers happy with a smooth sign-up. Moreover, studies show that long and cumbersome onboarding processes can cause up to 40% of potential customers to abandon the process (source danaconnect.com), so streamlining KYC is not just a cost issue but a revenue driver (fewer dropped applications). On the cost side, McKinsey reports that banks leading in end-to-end KYC automation have reduced KYC operational costs by 20–30%, while improving the quality of reviews and risk detection significantly (source mckinsey.com). In other words, less manual work and better compliance outcomes – a win-win. These automated ID verification flows also result in fewer false positives and errors, making regulatory compliance more robust. In sum, AI + documents + biometrics = secure, lightning-fast onboarding, a win-win for banks, insurers, and customers alike.

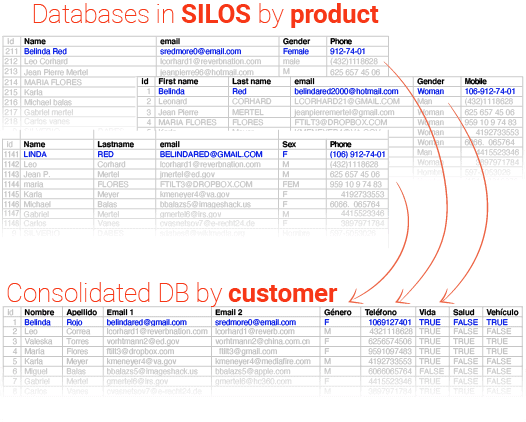

Automatic Document Reconciliation and Validation

Across internal operations, there are numerous tasks involving reconciling documents and cross-checking information. For instance, when a bank processes a mortgage, the file contains dozens of documents – application forms, credit reports, property appraisals, income statements, etc. A risk analyst traditionally had to verify that what the applicant stated matches the supporting documents, that the numbers add up, signatures are present, and so on. In insurance, consider reinsurance or internal audits: one needs to match policy terms with claims, or medical reports with coverage details, hunting for any discrepancies. These reconciliation tasks are tedious and error-prone for humans, especially after hours of review. AI can relieve this burden: IDP systems can read all the documents in a case and extract key fields (names, dates, amounts) and then automatically compare them to detect inconsistencies. For example, if one document lists a policy number that doesn’t match another, the system flags it. Or if the sum of attached invoices exceeds the policy’s coverage limit, it’s caught instantly. In accounting and operations, AI-driven automation is already performing things like bank reconciliations and payment matching autonomously – linking each invoice or receipt to the corresponding transaction. Deloitte has reported cases where AI helped with reconciliation and internal controls, simplifying operations and reducing manual workloads. The upshot is that companies can ensure information consistency and accuracy almost in real time, something that used to require teams of reviewers scrambling at month-end or year-end. And by automating these routine checks, errors drop and staff are freed to focus on higher-value analysis (for example, investigating only the truly anomalous cases instead of eyeballing every single file).

These are just a few examples. We could also mention underwriting automation (AI models evaluating risk by reading medical reports or property photos), or predictive analytics applied to historical documents to predict which claims might become complex or which clients might churn. In all these cases, intelligent automation accelerates cycle times, cuts costs, and improves accuracy – translating into tangible competitive advantages.

Importantly, the biggest value often comes when entire workflows are transformed end-to-end, not just small tasks in isolation. McKinsey points out that implementing isolated use cases (a chatbot here, a fraud detector there) does bring benefits, but a holistic reinvention of an entire process (say, the whole claims management journey) can yield up to 14 times more impact than the sum of individual point solutions (source mckinsey.com). This is due to synergies: when different automations are linked and reinforce each other, the resulting system is far more efficient and cohesive than each piece alone. The lesson for organizations is to think big and holistically – identify entire domains (claims, onboarding, compliance, etc.) and reinvent them end-to-end with AI, rather than deploying fragmented solutions that don’t “talk” to each other.

Conclusion: Preparing for the AI Transformation

The AI-driven transformation is already underway in the financial and insurance sector. We’ve seen how this new stage is redefining internal operations: AI can take over laborious document-based tasks, learning from unstructured data and making decisions faster than any human team could. In short, it’s boosting efficiency and business outcomes in ways traditional digital transformation alone couldn’t achieve.

However, capturing these benefits at scale isn’t automatic. What should insurers and banks do to lead (or at least not be left behind) in this shift toward an “AI transformation”? Based on industry studies and real-world experience, a few practical recommendations emerge:

1. Define a broad vision focused on business value: AI projects shouldn’t be mere one-off innovation experiments; they should tie into a strategic vision. The most advanced leaders view AI not just as a tool to cut costs, but also as a means to increase revenue and improve customer and employee experiences. Rather than adopting AI for the sake of AI, they anchor it to business outcomes. Identify in your organization which processes or domains, if boosted by AI, would generate the most value. For example, speeding up claims might improve customer satisfaction (NPS) and retention, or automating KYC might enable faster customer growth while staying compliant. In other words, start with the business problem/opportunity, not with the technology. As McKinsey and others note, the real payoff comes when AI is used to fundamentally reinvent key activities, not just to shave a few seconds off existing steps (source mckinsey.com).

2. Transform end-to-end, and avoid “pilot purgatory”: It’s tempting to start with very narrow use cases (a little chatbot here, a pilot there). Small pilots are fine to learn, but the goal should be to scale AI across the enterprise. Leading organizations resist getting comfortable with a handful of small successes; instead, they reimagine entire domains with multiple interconnected use cases (source mckinsey.com). If you’ve already done a successful proof-of-concept (say, using AI to extract data from invoices), think how to integrate that into the full workflow (e.g., automatic reconciliation, posting to the ledger, notifying the client, etc.). Don’t let your AI projects languish in perpetual pilot mode. Chart a path to full production implementation. This might mean phasing the rollout, but always with the endgame in mind – a fully transformed process, not just a cool demo. In short, avoid the “pilot purgatory” trap and plan for enterprise-wide adoption.

3. Invest in data, technology, and talent (appropriately): An effective AI transformation rests on solid foundations. That means quality data (structured and unstructured) that is accessible and well-governed; it may require modernizing platforms and moving to the cloud if needed, to ensure you have the infrastructure to scale AI models. Equally important is investing in talent and change management. Your business people need to understand these new tools’ capabilities (and limitations), and your tech people need to understand business priorities. Many successful organizations mention that managing change and training people consumes as much effort as building the technical solution. McKinsey’s experience suggests companies should invest at least as much in change management and user adoption as in the technology itself (source mckinsey.com). Employees need to trust and embrace the AI systems for them to deliver full value. This means upskilling staff to work alongside AI – redeploying them from rote tasks to higher-value roles – and cultivating a culture that sees AI as a collaborator, not a threat. Remember: AI isn’t there to replace human judgment, but to augment it. By freeing your teams from repetitive drudgery, you enable them to contribute where humans excel – in creativity, critical thinking, and empathy.

4. Governance and responsibility: When automating decisions and processes – especially in finance and insurance – it’s crucial to ensure responsibility, ethics, and compliance. Implementing Responsible AI practices means having controls to avoid biases in algorithms, protecting customer privacy, and adhering to regulations. Industry leaders advocate establishing AI governance frameworks early on, with involvement from risk, legal, and compliance teams. This helps build trust in the technology, both internally and externally. As Accenture emphasizes, trust is the foundation for unlocking AI’s full potential. In fact, 77% of executives globally (and 82% in Spain) believe the true benefits of AI will only be realized if built on a foundation of trust (source accenture.es). If employees and customers trust the AI-driven systems, they will embrace them; if not, there will be resistance and friction. So alongside every AI deployment, set clear policies, ensure transparency (e.g. explainable AI where relevant), and keep human oversight in the loop for critical decisions. A robust governance framework isn’t a “nice to have” – it’s essential for sustainable AI transformation.

In summary, digital transformation has evolved. Today, the cutting edge for banks and insurers is to embrace AI in the back-office, where operational efficiency and service excellence are at stake. Consulting firms like Deloitte talk about redefining “digital” as the core of business growth – now turbocharged by artificial intelligence. The companies that boldly integrate AI (while doing so responsibly) will be the ones setting the industry’s pace in the coming years. Those that remain in the comfort zone of traditional processes risk seeing their competitiveness erode as the productivity gap widens.

The invitation is clear: identify that cumbersome document-based process everyone in your organization groans about, and set out to transform it with AI. Start with a strong use case (you have plenty of examples: claims, KYC, reconciliations…), but always keep the broader vision in mind. Ensure you have the data, technology, and people readiness, and don’t forget to manage the cultural change. If you take these steps, you’ll soon see why this new phase of AI-driven transformation is not just a buzzword, but the real lever to elevate your company’s efficiency and innovation to the next level. Ultimately, it’s not about adopting AI to follow a trend – it’s about building more agile, intelligent, and customer-centric organizations that are poised to thrive in the era of artificial intelligence.